The airline industry is rising to unparalleled heights. Despite the scars of the pandemic, the blue sky is offering immense opportunities. A shining instance is King Abdul Aziz Airport in the Kingdom of Saudi Arabia, which welcomed more than 53 million passengers in 2025 in its history, a milestone reflecting traveler’s eagerness to experience desert safari and stargazing.

The number of passengers at different airports is just a single achievement in a larger sky. Globally, the aviation industry broke all previous records in 2025. According to the International Air Transport Association or IATA, a global and leading trading association, net profit is at an all-time high of $39.5 billion compared to the pre-pandemic period of $26 billion in 2019. The actual profitability is slightly below the industry estimates of $40 billion for 2026, which highlights a strong recovery driven by robust demand and operational efficiencies.

A quick review of 2024 showed that airlines served 4.8 billion passengers, surpassing the 2019 prep-pandemic record. In 2026, the numbers are expected to jump to almost 5 billion, showing the desire of passengers to reconnect, explore, and vacation. In 2025, the collective airline industry revenues exceeded the $1 trillion target and reached $1.008 trillion, a historically high figure. Revenue from tickets is $716 billion due to supplementary fees, such as baggage, while upgrades of seat helped earning billions. Airlines need more aircraft due to bolstered demand. The load factor (percentage of seats filled) is expected to reach 83% in 2026 that help achieve efficiency and profitability.

This post-pandemic improvement isn’t achieved overnight. Globally, airlines have dealt with labor shortages, escalated fuel costs, and regulatory bottlenecks to rise stronger. High load factor for airlines means full capacity airplanes, sound balance sheets, and sparkling profitability of $67 billion in 2025.

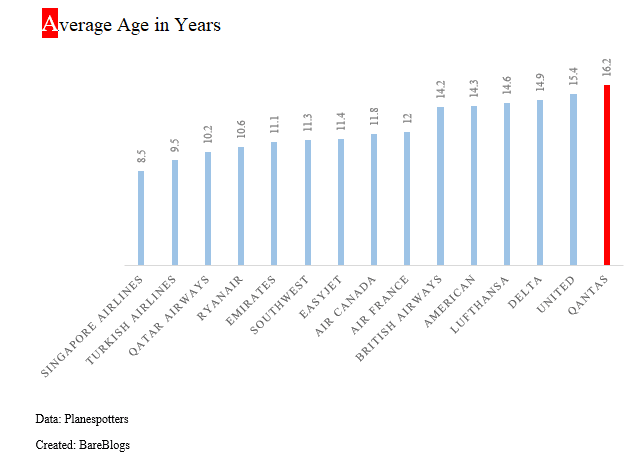

Experienced travelers know they will not always get smooth skies. The industry has a bank of challenges to avoid hurting the wings. Supply chain problems delay aircraft deliveries, which increases the fleet’s age and maintenance backlogs. An average airplane now ages more than 15 years in some areas. Asian and Middle Eastern carriers like Singapore Airlines and Turkish Airlines tend to have younger fleets, while some legacy carriers like Qantas and United operate older ones on average.

Geopolitical tensions due to airspace closures to GNSS interference force airlines to reroutes or face disruption, both of which are costly. Higher labor cost (wages exceeding productivity), airport fees, and shortage of spare parts, all enfolding margins to 3.9%.

There are also environmental pressures that extended burden. Airlines are required to use sustainable aviation fuel under arrangements like ReFuelEU and CORSIA, which will require them to spend billions to achieve compliance. Sustainable fuel, which is 0.8% of fuel utilization in 2026, will also be scarce due to production constraints. Slow global trade (0.5% forecasted for 2026) reduces cargo revenues, whereas policy uncertainties (possible tariffs and passenger rights expansions) increase regulatory red tape. North America has pilot shortages and limited infrastructure, while Africa’s growing unit costs reflect fragmented markets and infrastructure cracks.

Despite these high winds, the outlook is positive. Airlines are making efforts to improve efficiency, sustainability, and customer experience. Travelers can get better service and experience, though better routes and competitive rates are not guaranteed. So if you are planning for a vacation or scheduling a business trip, the aviation industry is ready to take off in 2026 after a record year.

To further read about strategic failures in aviation industry, read our premium blogs “PIA, a Pandora of Strategic Failures” and “Is PIA’s privatization fair?”